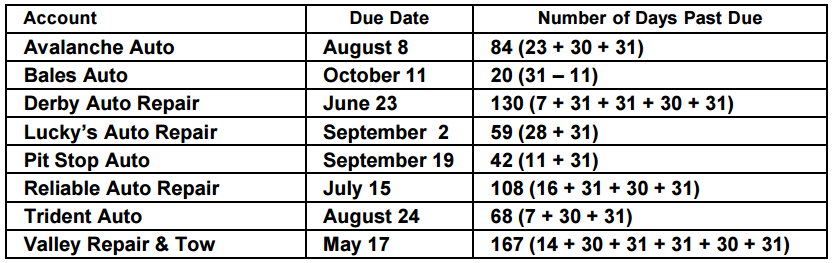

Toot Auto Supply distributes new and used automobile parts to local dealers throughout the Midwest. Toot’s credit terms are n/30. As of the end of business on October 31, the following accounts receivable were past due: Account Due Date AmountAvalanche Auto August 8 $12,000Bales Auto October 11 2,400Derby Auto Repair June 23 3,900Lucky’s Auto Repair September 2 6,600Pit Stop Auto September 19 1,100Reliable Auto Repair July 15 9,750Trident Auto August 24 1,800Valley Repair & Tow May 17 4,000Determine the number of days each account is past due as of October 31.Answer:

Account Due Date AmountAvalanche Auto August 8 $12,000Bales Auto October 11 2,400Derby Auto Repair June 23 3,900Lucky’s Auto Repair September 2 6,600Pit Stop Auto September 19 1,100Reliable Auto Repair July 15 9,750Trident Auto August 24 1,800Valley Repair & Tow May 17 4,000Determine the number of days each account is past due as of October 31.Answer: Account Due Date Number of Days Past DueAvalanche Auto August 8 84 (23 + 30 + 31)Bales Auto October 11 20 (31 – 11)Derby Auto Repair June 23 130 (7 + 31 + 31 + 30 + 31)Lucky’s Auto Repair September 2 59 (28 + 31)Pit Stop Auto September 19 42 (11 + 31)Reliable Auto Repair July 15 108 (16 + 31 + 30 + 31)Trident Auto August 24 68 (7 + 30 + 31)Valley Repair & Tow May 17 167 (14 + 30 + 31 + 31 + 30 + 31)

Account Due Date Number of Days Past DueAvalanche Auto August 8 84 (23 + 30 + 31)Bales Auto October 11 20 (31 – 11)Derby Auto Repair June 23 130 (7 + 31 + 31 + 30 + 31)Lucky’s Auto Repair September 2 59 (28 + 31)Pit Stop Auto September 19 42 (11 + 31)Reliable Auto Repair July 15 108 (16 + 31 + 30 + 31)Trident Auto August 24 68 (7 + 30 + 31)Valley Repair & Tow May 17 167 (14 + 30 + 31 + 31 + 30 + 31)

The accounts receivable clerk for Thunderwood Industries prepared the following partially completed aging of receivables schedule as of the end of business on August 31: NotDuePast90OverCustomer BalanceDays Past DueAllied Industries Inc.Archer CompanyZussman CompanySubtotals 3,0004,5005,000750,000 7,0005,00075,0003,000480,0004,500160,000 28,000The following accounts were unintentionally omitted from the aging schedule and not included in the subtotals above:

NotDuePast90OverCustomer BalanceDays Past DueAllied Industries Inc.Archer CompanyZussman CompanySubtotals 3,0004,5005,000750,000 7,0005,00075,0003,000480,0004,500160,000 28,000The following accounts were unintentionally omitted from the aging schedule and not included in the subtotals above:

Customer Balance Due DateColor World Industries $33,000 March 13Hawks Company 15,000 June 29Osler Inc. 21,000 July 8Sather Sales Company 8,000 September 6Wisdom Company 6,500 August 25a. Determine the number of days past due for each of the preceding accounts as of August 31.b. Complete the aging of receivables schedule by adding the omitted accounts to the bottom of the schedule and updating the totals.Answer: a. Customer Due Date Number of Days Past DueColor World Industries March 13 171 days (18 + 30 + 31 + 30 + 31 + 31)Hawks Company June 29 63 days (1 + 31 + 31)Osler Inc. July 8 54 days (23 + 31)Sather Sales Company September 6 Not past dueWisdom Company August 25 6 days (31 – 25)

a. Customer Due Date Number of Days Past DueColor World Industries March 13 171 days (18 + 30 + 31 + 30 + 31 + 31)Hawks Company June 29 63 days (1 + 31 + 31)Osler Inc. July 8 54 days (23 + 31)Sather Sales Company September 6 Not past dueWisdom Company August 25 6 days (31 – 25)

b. Aging of Receivables ScheduleAugust 31Customer BalanceNot PastDueDays Past Due1–30 31–60 61–90Over90Allied Industries Inc. 3,000 3,000Archer Company 4,500 4,500Zussman Company 5,000 5,000Subtotals 750,000 480,000 160,000 75,000 28,000 7,000Color World Industries 33,000 33,000Hawks Company 15,000 15,000Osler Inc. 21,000 21,000Sather Sales Company 8,000 8,000Wisdom Company 6,500 6,500Totals 833,500 488,000 166,500 96,000 43,000 40,000

Thunderwood Industries has a past history of uncollectible accounts, as shown below. Estimate the allowance for doubtful accounts, based on the aging of receivables schedule you completed in Exercise 9-8. Age ClassPercentUncollectibleNot past due 2%1–30 days past due 631–60 days past due 1261–90 days past due 30Over 90 days past due 75Answer:

Age ClassPercentUncollectibleNot past due 2%1–30 days past due 631–60 days past due 1261–90 days past due 30Over 90 days past due 75Answer:

BalanceNot PastDueDays Past Due1–30 31–60 61–90Over90Total receivables 833,500 488,000 166,500 96,000 43,000 40,000Percentage uncollectible 2% 6% 12% 30% 75%Allowance for doubtfulaccounts 74,170 9,760 9,990 11,520 12,900 30,000

Traditional Bikes Co. is a wholesaler of motorcycle supplies. An aging of the company’s accounts receivable on December 31, 2014, and a historical analysis of the percentage of uncollectible accounts in each age category are as follows: Age Interval BalancePercentUncollectibleNot past due $ 740,000 ½%1–30 days past due 390,000 231–60 days past due 85,000 461–90 days past due 28,000 1491–180 days past due 42,000 32Over 180 days past due 15,000 80$1,300,000Estimate what the proper balance of the allowance for doubtful accounts should be as of December 31, 2014.Answer:

Age Interval BalancePercentUncollectibleNot past due $ 740,000 ½%1–30 days past due 390,000 231–60 days past due 85,000 461–90 days past due 28,000 1491–180 days past due 42,000 32Over 180 days past due 15,000 80$1,300,000Estimate what the proper balance of the allowance for doubtful accounts should be as of December 31, 2014.Answer:

Age Interval BalanceEstimatedUncollectible AccountsPercent AmountNot past due $ 740,000 0.5% $ 3,7001–30 days past due 390,000 2% 7,80031–60 days past due 85,000 4% 3,40061–90 days past due 28,000 14% 3,92091–180 days past due 42,000 32% 13,440Over 180 days past due 15,000 80% 12,000Total $1,300,000 $44,260

Using the data in Exercise 9-11, assume that the allowance for doubtful accounts for Traditional Bikes Co. had a debit balance of $3,375 as of December 31, 2014. Journalize the adjusting entry for uncollectible accounts as of December 31, 2014.Answer: 2014Dec. 31 Bad Debt Expense 47,635Allowance for Doubtful Accounts 47,635Uncollectible accounts estimate($44,260 + $3,375).

2014Dec. 31 Bad Debt Expense 47,635Allowance for Doubtful Accounts 47,635Uncollectible accounts estimate($44,260 + $3,375).

The following selected transactions were taken from the records of Shipway Company for the first year of its operations ending December 31, 2014:Apr. 13. Wrote off account of Dean Sheppard, $8,450.May 15. Received $500 as partial payment on the $7,100 account of Dan Pyle. Wrote off the remaining balance as uncollectible.July 27. Received $8,450 from Dean Sheppard, whose account had been written off onApril 13. Reinstated the account and recorded the cash receipt.Dec. 31. Wrote off the following accounts as uncollectible (record as one journal entry): Paul Chapman $2,225Duane DeRosa 3,550Teresa Galloway 4,770Ernie Klatt 1,275Marty Richey 1,69031. If necessary, record the year-end adjusting entry for uncollectible accounts.a. Journalize the transactions for 2014 under the direct write-off method.b. Journalize the transactions for 2014 under the allowance method. Shipway Company uses the percent of credit sales method of estimating uncollectible accounts expense. Based on past history and industry averages, ¾% of credit sales are expected to be uncollectible. Shipway Company recorded $3,778,000 of credit sales during 2014.c. How much higher (lower) would Shipway Company’s net income have been under the direct write-off method than under the allowance method?Answer:

Paul Chapman $2,225Duane DeRosa 3,550Teresa Galloway 4,770Ernie Klatt 1,275Marty Richey 1,69031. If necessary, record the year-end adjusting entry for uncollectible accounts.a. Journalize the transactions for 2014 under the direct write-off method.b. Journalize the transactions for 2014 under the allowance method. Shipway Company uses the percent of credit sales method of estimating uncollectible accounts expense. Based on past history and industry averages, ¾% of credit sales are expected to be uncollectible. Shipway Company recorded $3,778,000 of credit sales during 2014.c. How much higher (lower) would Shipway Company’s net income have been under the direct write-off method than under the allowance method?Answer:

a. Apr. 13 Bad Debt Expense 8,450Accounts Receivable—Dean Sheppard 8,450May 15 Cash 500Bad Debt Expense 6,600Accounts Receivable—Dan Pyle 7,100July 27 Accounts Receivable—Dean Sheppard 8,450Bad Debt Expense 8,45027 Cash 8,450Accounts Receivable—Dean Sheppard 8,450Dec. 31 Bad Debt Expense 13,510Accounts Receivable—Paul Chapman 2,225Accounts Receivable—Duane DeRosa 3,550Accounts Receivable—Teresa Galloway 4,770Accounts Receivable—Ernie Klatt 1,275Accounts Receivable—Marty Richey 1,69031 No entry b. Apr. 13 Allowance for Doubtful Accounts 8,450Accounts Receivable—Dean Sheppard 8,450May 15 Cash 500Allowance for Doubtful Accounts 6,600Accounts Receivable—Dan Pyle 7,100July 27 Accounts Receivable—Dean Sheppard 8,450Allowance for Doubtful Accounts 8,45027 Cash 8,450Accounts Receivable—Dean Sheppard 8,450Dec. 31 Allowance for Doubtful Accounts 13,510Accounts Receivable—Paul Chapman 2,225Accounts Receivable—Duane DeRosa 3,550Accounts Receivable—Teresa Galloway 4,770Accounts Receivable—Ernie Klatt 1,275Accounts Receivable—Marty Richey 1,69031 Bad Debt Expense 28,335Allowance for Doubtful Accounts 28,335Uncollectible accounts estimate($3,778,000 × 0.75% = $28,335).

b. Apr. 13 Allowance for Doubtful Accounts 8,450Accounts Receivable—Dean Sheppard 8,450May 15 Cash 500Allowance for Doubtful Accounts 6,600Accounts Receivable—Dan Pyle 7,100July 27 Accounts Receivable—Dean Sheppard 8,450Allowance for Doubtful Accounts 8,45027 Cash 8,450Accounts Receivable—Dean Sheppard 8,450Dec. 31 Allowance for Doubtful Accounts 13,510Accounts Receivable—Paul Chapman 2,225Accounts Receivable—Duane DeRosa 3,550Accounts Receivable—Teresa Galloway 4,770Accounts Receivable—Ernie Klatt 1,275Accounts Receivable—Marty Richey 1,69031 Bad Debt Expense 28,335Allowance for Doubtful Accounts 28,335Uncollectible accounts estimate($3,778,000 × 0.75% = $28,335).

c. Bad debt expense under:Allowance method………………………...……………………………………… $28,335Direct write-off method ($8,450 + $6,600 – $8,450 + $13,510)…………… 20,110Difference ($28,335 – $20,110)………………………………………………… $ 8,225Shipway Company’s income would be $8,225 higher under the direct write-offmethod than under the allowance method.

During its first year of operations, Mack’s Plumbing Supply Co. had net sales of $3,250,000, wrote off $27,800 of accounts as uncollectible using the direct write-off method, and reported net income of $487,500. Determine what the net income would have been if the allowance method had been used, and the company estimated that 1% of net sales would be uncollectible.Answer:$482,800 [$487,500 + $27,800 – ($3,250,000 × 1%)]

The following selected transactions were taken from the records of Rustic Tables Company for the year ending December 31, 2014:June 8. Wrote off account of Kathy Quantel, $8,440.Aug. 14. Received $3,000 as partial payment on the $12,500 account of Rosalie Oakes. Wrote off the remaining balance as uncollectible.Oct. 16. Received the $8,440 from Kathy Quantel, whose account had been written off on June 8. Reinstated the account and recorded the cash receipt.Dec. 31. Wrote off the following accounts as uncollectible (record as one journal entry):

Wade Dolan $4,600Greg Gagne 3,600Amber Kisko 7,150Shannon Poole 2,975Niki Spence 6,63031. If necessary, record the year-end adjusting entry for uncollectible accounts.a. Journalize the transactions for 2014 under the direct write-off method.b. Journalize the transactions for 2014 under the allowance method, assuming that the allowance account had a beginning balance of $36,000 on January 1, 2014, and the company uses the analysis of receivables method. Rustic Tables Company prepared the following aging schedule for its accounts receivable: Aging Class (Numberof Days Past Due)Receivables Balanceon December 31Estimated Percent ofUncollectible Accounts0–30 days $320,000 1%31–60 days 110,000 361–90 days 24,000 1091–120 days 18,000 33More than 120 days 43,000 75Total receivables $515,000c. How much higher (lower) would Rustic Tables’ 2014 net income have been under the direct write-off method than under the allowance method?Answer:

Aging Class (Numberof Days Past Due)Receivables Balanceon December 31Estimated Percent ofUncollectible Accounts0–30 days $320,000 1%31–60 days 110,000 361–90 days 24,000 1091–120 days 18,000 33More than 120 days 43,000 75Total receivables $515,000c. How much higher (lower) would Rustic Tables’ 2014 net income have been under the direct write-off method than under the allowance method?Answer: a. June 8 Bad Debt Expense 8,440Accounts Receivable—Kathy Quantel 8,440Aug. 14 Cash 3,000Bad Debt Expense 9,500Accounts Receivable—Rosalie Oakes 12,500Oct. 16 Accounts Receivable—Kathy Quantel 8,440Bad Debt Expense 8,44016 Cash 8,440Accounts Receivable—Kathy Quantel 8,440Dec. 31 Bad Debt Expense 24,955Accounts Receivable—Wade Dolan 4,600Accounts Receivable—Greg Gagne 3,600Accounts Receivable—Amber Kisko 7,150Accounts Receivable—Shannon Poole 2,975Accounts Receivable—Niki Spence 6,63031 No entry

a. June 8 Bad Debt Expense 8,440Accounts Receivable—Kathy Quantel 8,440Aug. 14 Cash 3,000Bad Debt Expense 9,500Accounts Receivable—Rosalie Oakes 12,500Oct. 16 Accounts Receivable—Kathy Quantel 8,440Bad Debt Expense 8,44016 Cash 8,440Accounts Receivable—Kathy Quantel 8,440Dec. 31 Bad Debt Expense 24,955Accounts Receivable—Wade Dolan 4,600Accounts Receivable—Greg Gagne 3,600Accounts Receivable—Amber Kisko 7,150Accounts Receivable—Shannon Poole 2,975Accounts Receivable—Niki Spence 6,63031 No entry b. June 8 Allowance for Doubtful Accounts 8,440Accounts Receivable—Kathy Quantel 8,440Aug. 14 Cash 3,000Allowance for Doubtful Accounts 9,500Accounts Receivable—Rosalie Oakes 12,500Oct. 16 Accounts Receivable—Kathy Quantel 8,440Allowance for Doubtful Accounts 8,44016 Cash 8,440Accounts Receivable—Kathy Quantel 8,440Dec. 31 Allowance for Doubtful Accounts 24,955Accounts Receivable—Wade Dolan 4,600Accounts Receivable—Greg Gagne 3,600Accounts Receivable—Amber Kisko 7,150Accounts Receivable—Shannon Poole 2,975Accounts Receivable—Niki Spence 6,63031 Bad Debt Expense 45,545Allowance for Doubtful Accounts 45,545Uncollectible accounts estimate($47,090 – $1,545).Computations:Aging Class(Number of DaysPast Due)ReceivablesBalance onDecember 31Estimated DoubtfulAccountsPercent Amount0–30 days $320,000 1% $ 3,20031–60 days 110,000 3% 3,30061–90 days 24,000 10% 2,40091–120 days 18,000 33% 5,940More than 120 days 43,000 75% 32,250Total receivables $515,000 $47,090Estimated balance of allowance account from aging schedule…………………… $47,090Unadjusted credit balance of allowance account*…………………………………… 1,545Adjustment………………………………………………………………………………… $45,545* $36,000 – $8,440 – $9,500 + $8,440 – $24,955 = $1,545

b. June 8 Allowance for Doubtful Accounts 8,440Accounts Receivable—Kathy Quantel 8,440Aug. 14 Cash 3,000Allowance for Doubtful Accounts 9,500Accounts Receivable—Rosalie Oakes 12,500Oct. 16 Accounts Receivable—Kathy Quantel 8,440Allowance for Doubtful Accounts 8,44016 Cash 8,440Accounts Receivable—Kathy Quantel 8,440Dec. 31 Allowance for Doubtful Accounts 24,955Accounts Receivable—Wade Dolan 4,600Accounts Receivable—Greg Gagne 3,600Accounts Receivable—Amber Kisko 7,150Accounts Receivable—Shannon Poole 2,975Accounts Receivable—Niki Spence 6,63031 Bad Debt Expense 45,545Allowance for Doubtful Accounts 45,545Uncollectible accounts estimate($47,090 – $1,545).Computations:Aging Class(Number of DaysPast Due)ReceivablesBalance onDecember 31Estimated DoubtfulAccountsPercent Amount0–30 days $320,000 1% $ 3,20031–60 days 110,000 3% 3,30061–90 days 24,000 10% 2,40091–120 days 18,000 33% 5,940More than 120 days 43,000 75% 32,250Total receivables $515,000 $47,090Estimated balance of allowance account from aging schedule…………………… $47,090Unadjusted credit balance of allowance account*…………………………………… 1,545Adjustment………………………………………………………………………………… $45,545* $36,000 – $8,440 – $9,500 + $8,440 – $24,955 = $1,545 c. Bad debt expense under:Allowance method………………………………………………………………… $45,545Direct write-off method ($8,440 + $9,500 – $8,440 + $24,955)…………… 34,455Difference………………………………………………………………………… $11,090Rustic Tables’ income would be $11,090 higher under the direct write-off methodthan under the allowance method.

c. Bad debt expense under:Allowance method………………………………………………………………… $45,545Direct write-off method ($8,440 + $9,500 – $8,440 + $24,955)…………… 34,455Difference………………………………………………………………………… $11,090Rustic Tables’ income would be $11,090 higher under the direct write-off methodthan under the allowance method.

Using the data in Exercise 9-15, assume that during the second year of operations Mack’s Plumbing Supply Co. had net sales of $4,100,000, wrote off $34,000 of accounts as uncollectible using the direct write-off method, and reported net income of $600,000.a. Determine what net income would have been in the second year if the allowance method (using 1% of net sales) had been used in both the first and second years.b. Determine what the balance of the allowance for doubtful accounts would have been at the end of the second year if the allowance method had been used in both the first and second years.Answer:a. $593,000 [$600,000 + $34,000 – ($4,100,000 × 1%)]b. $11,700 ($32,500 – $27,800) + ($41,000 – $34,000)

{kind=link}

{kind=link}